It was the fall of 2015, and our College Possible team was excited to begin pursuit of a big, hairy, audacious goal to improve our college graduation rate. In order to achieve this goal, we began to examine all aspects of our programming and operations to see how we could improve the college success of our students. In particular, we tried to identify some key levers that could help us make dramatic leaps in persistence and graduation rates.

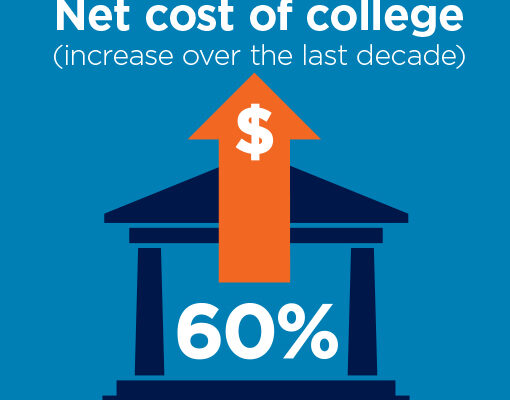

Not surprisingly, affordability quickly arose as one of the primary challenges to student success. During this process, I came across a key statistic that has stuck with me: the net cost of college to students and families has increased 60 percent over the last decade. Can you think of a single other good or service, with the possible exception of health care, that has seen such dramatic increases? Do you know many families whose resources have increased at a similar rate? Doesn’t it also stand to reason, then, that this incredible rise in cost would also have an important impact on degree-seeking and earning, especially for low-income families?

The time frame of that statistic also struck me, because I had been in my seat as the head of programming at College Possible for a little over a decade. In my early days with the organization, in the mid-2000s, I often said with confidence that if we did our job right, and our students followed our guidance, they could find a college pathway where finances did not have to be a barrier to success.

A decade later, I can no longer say the same thing. In 2018, we can do everything right, our students can follow all our best advice, and they can still find themselves without an affordable college option that gives them a good chance of earning their degree within six years. In a recent assessment conducted on student financial aid and financial decisions, we found that even with comprehensive financial aid packages and subsidized loans, the gap in College Possible students’ available funds and the total cost of college attendance is more than $4,000 per year. While that may seem like a small amount on the surface, for the average student in our program that represents about 15 percent of their family’s annual income. Our first key lever had emerged: helping our students find affordable pathways to a bachelor’s degree.

To this end, we are now trying many things: improving our financial literacy coaching for students; working intensively with college partners; getting involved in advocacy work around financial aid; and identifying additional financial resources for students. One key idea we are testing, in partnership with the nonprofit Better Future Forward, is the development of an alternative funding model for students called an “income share agreement,” or ISA.

There are important policy critiques of the ISA concept, the most disquieting to College Possible being that, like any financial product, they can easily become far more beneficial for the provider than the low-income student using the funds. For that reason, it was extremely important for us to find a service provider we trusted to build a structure that is fair and transparent to the student user. Better Future Forward’s CEO, Kevin James, had been working for years on the concept of the ISA, and was interested in partnering with an organization specifically focused on serving low-income students to figure out how best to design an offering to help expand college opportunity for those who most need help in affording college. As an organization, we had our concerns, but in a quest to try a variety of innovative solutions and with the comfort that BFF would work with us to meet our students’ needs, we embarked on a pilot project.

In working with the BFF team, we designed a model that met several goals:

- It wouldn’t replace grants, scholarships or subsidized loans, but could be an option where students might otherwise take out a private loan, work too many hours to be successful in school, or drop out.

- It had to be transparent in helping students understand the agreement they were entering into.

- It protected students from taking on too much obligation for repayment, with this option alone as well as when combined with traditional student loan debt.

- It provided students and families with a knowledgeable advisor who could answer their questions, and a calculator that helped them compare ISAs to other financing options.

- It offered favorable terms for students, a key differentiator between financial instruments that create access versus those that are predatory toward ill-informed or desperate borrowers.

In the summer of 2017, we launched our initial pilot program in Minnesota. The opportunity to participate in an ISA was offered to students at six public and private colleges in Minnesota, across a variety of disciplines including humanities, social sciences, business and pre-professional programs. Seventy percent of students who applied for funding indicated that they needed additional resources beyond what the university was able to offer to be able to continue in school. Of those offered the funding, 15 chose to accept an average amount of $6,800; others decided not to participate, suggesting that students had ample information and free choice to participate or not, based on their own circumstances. As one participant noted, “It’s really nice that people are thinking about alternative options in terms of student loans. The debt burden for me was really scary, but you don’t want to not invest in yourself.”

We will continue to follow these students until graduation, and hope to expand this pilot to a size that helps us draw more meaningful conclusions about the relationship between the ISA offering and student success.

The ISA is a model that generates both interest and skepticism. We share many of those concerns about the policy implications of the wide-scale offering of ISAs, and see the potential for harm to uninformed consumers, just as there is with all financial products. Many people would rather see additional resources put into scholarships or state-based funding to keep the cost of college down, and we agree with those goals as well. But we also know the challenge of affordability will exist for low-income students into the foreseeable future, and while we pursue policies to reduce the incredible cost of college, we need mechanisms to help students in the meantime. We’re excited about the opportunity to provide this option for some students who would find it valuable, while contributing to the learning in the field about what is needed to ensure ISAs are built with low-income student success as the primary goal.